Painstaking years of mortgage repayment

Imagine diligently paying down your mortgage, year after painstaking year, believing you’re making the smartest financial move for your future. What if I told you that, for many Canadian homeowners, this conventional wisdom is costing them thousands in missed tax deductions and untapped wealth accumulation? In a financial landscape where every dollar counts, a passive approach to your largest household debt isn't just inefficient; it's a significant financial oversight that can silently erode your potential for true financial independence. The fear isn't just about missing an opportunity; it's about actively losing ground, subjecting your hard-earned money to unnecessary tax burdens while others strategically leverage their assets for greater returns.

This isn't about risky gambles or shady schemes. It's about understanding the sophisticated tax strategies available to you, strategies that turn your mortgage from a liability into a powerful engine for wealth creation. If the thought of paying off your mortgage faster while simultaneously generating tax-deductible investment income sounds too good to be true, you're not alone. But the reality is, a legitimate and powerful strategy exists: the Smith Maneuver. This can fundamentally transform your financial trajectory in Canada. Ignoring it means resigning yourself to the status quo, watching potential tax refunds and investment gains pass you by, all while your mortgage interest remains stubbornly undeductible.

The Invisible Burden of Non-Deductible Mortgage Interest

For many Canadians, the largest debt they will ever carry is their home mortgage. Unlike our neighbours to the south, Canada generally does not allow homeowners to deduct mortgage interest from their taxable income. This fundamental difference creates a silent, yet substantial, financial burden. Every dollar you pay in mortgage interest is paid with after-tax income, representing a significant cash outflow that offers no immediate tax relief. Over the lifespan of a 25- or 30-year mortgage, this can amount to tens, if not hundreds, of thousands of dollars that simply disappear into the loan, rather than being redirected to build your personal wealth.

This isn't merely an inconvenience; it's a dead weight on your financial progress. Think of it as a constant drag on your net worth, a missed opportunity to retain more of your income, and a slower path to true financial freedom. The anxiety stems from knowing that while you're working hard to pay down debt, you're simultaneously missing out on a powerful mechanism for tax efficiency. This passive acceptance of non-deductible interest means your hard-earned money is working against you in terms of tax, rather than for you. It's a risk of financial stagnation, where your most significant asset, your home, isn't fully participating in your wealth-building strategy.

Misunderstanding Investment Loan Deductibility

The path to turning a liability into an asset is fraught with potential pitfalls if not navigated correctly. The key principle behind leveraging your mortgage for tax deductions lies in Canada's tax rules regarding investment loans: interest paid on money borrowed to earn investment income is generally tax-deductible. However, the line between personal debt and investment debt can be perilously thin, and a misstep can lead to severe compliance headaches and the complete loss of your intended tax benefits. Many homeowners, attempting to use their home equity in a casual manner, fail to properly segregate funds or document their transactions, inadvertently blurring the critical distinction required by the Canada Revenue Agency (CRA).

The danger here is not just losing the deduction; it's attracting unwanted scrutiny from tax authorities. Improperly claimed deductions, a lack of clear documentation, or commingling of funds can trigger audits, leading to reassessments, back taxes, and potentially significant interest and penalties. The cost of non-compliance can quickly outweigh any perceived benefits, transforming your well-intentioned strategy into a costly mistake. The anxiety intensifies when one considers the complexities of tracking investment loans, the specific requirements for proving intent to earn income, and the meticulous record-keeping essential to withstand CRA review. Without strict adherence to protocol, you risk having legitimate deductions disallowed and facing additional tax liabilities you never anticipated.

Optimizing Investment & Retirement Structuring

Once your mortgage is structured for the Smith Maneuver, the next critical phase involves the careful selection and management of your investment portfolio to maximize tax efficiency. This isn't a "set it and forget it" approach; it requires a strategic understanding of how different asset types are taxed in Canada and how to align them with your Smith Maneuver objectives. The goal is to generate taxable investment income against which your HELOC interest deductions can be applied, effectively reducing your overall taxable income and resulting in larger tax refunds.

For example, investing in dividend-paying stocks or interest-bearing instruments within a non-registered account can provide the necessary income streams. While Tax-Free Savings Accounts (TFSAs) are excellent for tax-sheltered growth, and Registered Retirement Savings Plans (RRSPs) offer tax deferral, the Smith Maneuver's deductions are best utilized against taxable income generated outside these registered plans. A nuanced strategy involves understanding how to balance these different account types alongside your leveraged investment. The aim is not just to invest, but to invest intelligently, ensuring that the income generated properly offsets your deductible interest, accelerating your mortgage payoff and overall wealth growth while carefully considering your risk appetite. For those nearing retirement, the Smith Maneuver can be a powerful tool to build wealth that supplements traditional retirement savings, but integrating it requires careful consideration of long-term tax implications and withdrawal strategies.

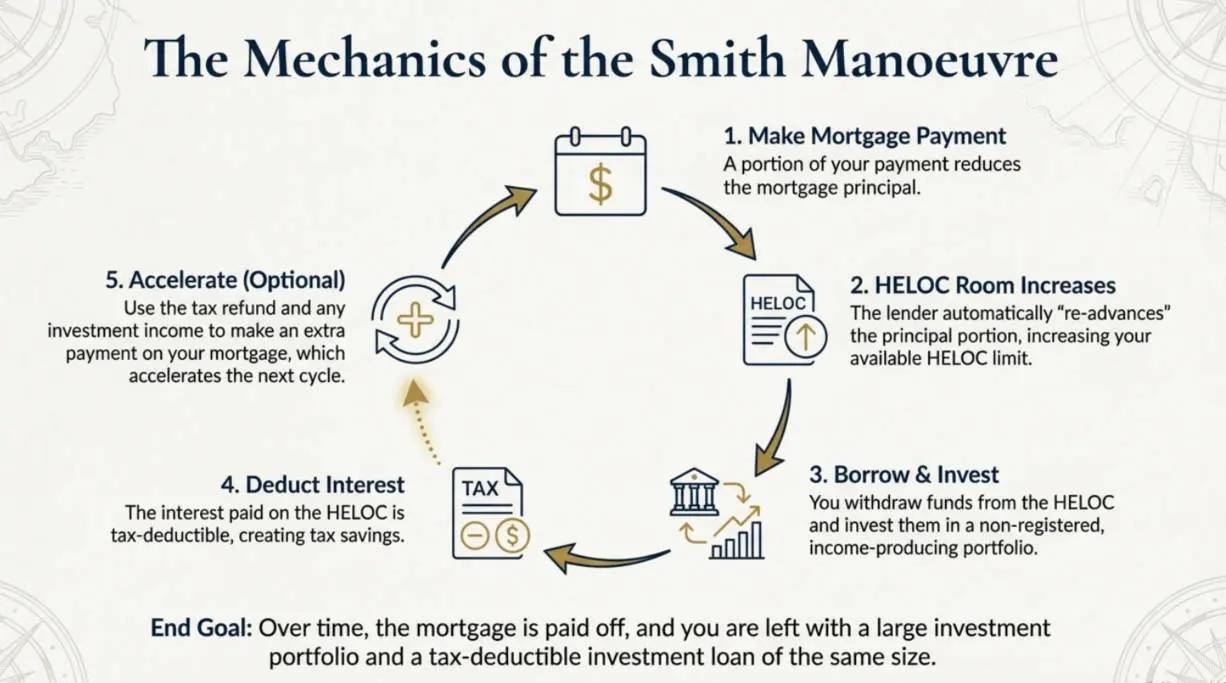

Architecting Your Mortgage into an Investment Powerhouse (The Smith Maneuver)

The foundational step to transforming your mortgage into a tax-efficient wealth-building tool is the precise application of the Smith Maneuver. This strategy involves converting non-deductible mortgage debt into tax-deductible investment debt. It's not about taking on more debt, but rather strategically restructuring your existing financial commitments. The core mechanism is a readvanceable mortgage, which combines your traditional mortgage with a Home Equity Line of Credit (HELOC). As you pay down the principal on your mortgage, the available credit limit on your HELOC automatically increases.

This ingenious design allows you to systematically borrow back the very principal you've paid off your mortgage, but crucially, these borrowed funds are then directly invested in income-generating assets. The interest paid on this specific HELOC portion becomes tax-deductible because the funds are explicitly used to generate investment income. This creates a powerful cycle: you chip away at your non-deductible mortgage principal, which simultaneously unlocks tax-deductible investment capital. This re-engineering of your financial structure is the first, most critical step in unlocking the benefits of tax-efficient investing directly linked to your home equity, laying the groundwork for accelerated wealth accumulation and significant tax relief.

The Power of Integrated, Evolving Compliance Protocols

Successfully implementing the Smith Maneuver extends far beyond the initial setup; it demands a rigorous, ongoing commitment to compliant execution and dynamic adaptation. This strategy is not a static solution; it's a living financial plan that must evolve with your life circumstances, market fluctuations, and tax law changes. The most critical component of this ongoing management is meticulous record-keeping. You must maintain impeccable documentation that clearly separates your personal mortgage payments from your HELOC drawdowns for investment purposes. Any commingling of funds or unclear trails can jeopardize the deductibility of your interest, potentially negating all the benefits.

This requires establishing robust, integrated compliance protocols, akin to a sophisticated financial system. You need a clear process for how HELOC funds are drawn, how they are invested, and how all related interest payments and investment income are tracked. This also means regularly reviewing your investment performance and adjusting your strategy as needed. Life events, such as a job change, a market downturn, or a shift in your risk tolerance, all necessitate a re-evaluation of your Smith Maneuver strategy. An integrated approach ensures that you're not just compliant today, but that your strategy remains robust and optimized for your evolving financial goals, providing continuous tax efficiency and peace of mind.

Cross-Border Tax Expert Guidance Matters

Cross-border tax planning is complicated, not a DIY project. The stakes are too high, and the nuances of Canadian and US tax laws, combined with the complexities of the tax treaty, are too great for generalized advice or online guesswork. A seasoned cross-border tax strategist can help you accurately determine your residency status, calculate and mitigate departure tax, navigate withholding taxes, and ensure all necessary forms (like T1161) are filed correctly and on time. At MFI, we translate jargon into clear, actionable advice, building a robust compliance strategy that protects your wealth and provides a clear roadmap for your financial future in Canada and the US. Don't let tax anxiety overshadow your new beginning – empower your move with expert cross-border tax planning.

Book Your Initial Cross-Border Tax Consultant