The Hidden Dangers of Foreign Corporation Reporting

Imagine building a thriving business, expanding your operations across the US-Canada border, and feeling confident about your hard-earned success. You've meticulously navigated market entries, dealt with cultural nuances, and are finally seeing your cross-border vision take shape. But what if there was an invisible threat lurking in your financial structure, one that could turn your entrepreneurial dreams into an IRS nightmare? For many U.S. citizens or residents involved with Canadian (or any foreign) corporations, a complex and often overlooked reporting requirement Form 5471.

You might be a founder, an executive, or a significant shareholder in a foreign entity, believing your corporate structure is sound. Yet, the IRS has a long memory and an even longer reach, extending its grasp to monitor the financial activities of U.S. persons globally. Ignoring these intricate rules isn't merely a minor oversight; it's a direct path to astronomical penalties, audits, and significant financial distress. The question isn't if you're subject to these rules, but whether you truly understand the perils and the proven strategies to navigate them successfully.

Trap of Worldwide Taxation for U.S. Persons

As a U.S. citizen or green card holder, you are subject to worldwide income taxation by the United States, regardless of where you live or where your income is earned. This fundamental principle extends its reach directly into your involvement with foreign corporations. Even if your company is legally established and operating solely in Canada, your status as a "U.S. person" (which can include officers, directors, or significant shareholders) means the IRS views your connection to that foreign entity through a specific, demanding lens.

This isn't just about paying tax on your personal income; it's about the IRS demanding transparency into the very fabric of your foreign corporation. Your ownership, even if indirect, pulls the foreign entity into the U.S. tax compliance orbit. This can create a disconnect where you believe your Canadian company is solely under Canadian jurisdiction, while the IRS silently expects detailed information about its finances, ownership, and transactions. Without specialized guidance, this foundational misunderstanding can lead to a cascade of overlooked obligations, setting the stage for severe consequences down the line.

Form 5471 and Astronomical Penalties

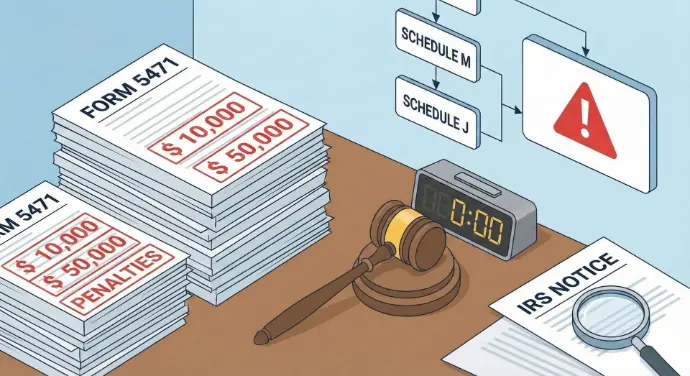

The IRS Form 5471, "Information Return of U.S. Persons With Respect To Certain Foreign Corporations," is arguably one of the most feared and complex international information returns for U.S. individuals and businesses engaged in cross-border activities. It’s designed to provide the IRS with a comprehensive look into the ownership, operations, and financial performance of foreign corporations that U.S. persons control or have significant interests in. The form itself is not a tax payment; it's purely an informational report, but its absence or incorrect filing triggers devastating penalties.

The stakes are astronomically high. The penalty for failing to file a complete and accurate Form 5471 is an initial $10,000 per information return, per year. This isn't a one-time fine; if you fail to file after the IRS notifies you, an additional $10,000 penalty accrues for each 30-day period (or fraction thereof) the failure continues, up to a maximum of $50,000 per return. Moreover, substantial penalties can also be imposed for understatements of tax attributable to non-disclosed foreign financial assets, and in cases of willful disregard, criminal penalties may even apply. This isn't just about missing a deadline; it’s about inadvertently exposing yourself to potentially crippling financial liabilities that can far outweigh any tax owed. Understanding the intricate schedules within Form 5471 (such as Schedule M for related party transactions or Schedule J for accumulated earnings) is crucial, as each provides a potential pitfall if not completed with extreme precision.

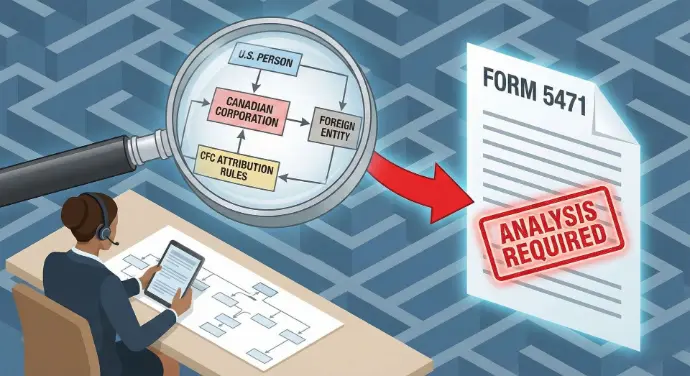

Proactive Entity Classification & Ownership Analysis

The first and most critical step in navigating the labyrinth of cross-border corporate compliance is a meticulous, expert-led analysis of your entity's classification and your ownership structure. Before you can even begin to address Form 5471, you must definitively determine if your Canadian corporation (or any foreign entity) triggers U.S. reporting requirements for you as a U.S. person. This involves more than just a cursory glance at your company registration. It demands a deep dive into definitions like "U.S. person," "foreign corporation," and "controlled foreign corporation" (CFC), which often involve complex attribution rules that can extend ownership far beyond direct equity holdings.

An experienced cross-border tax expert will help you dissect your specific situation, identifying all U.S. persons who are officers, directors, or meet certain shareholder thresholds (e.g., 10% or more ownership of vote or value, or aggregate 50% ownership for CFC status). This analysis clarifies not only if a Form 5471 is required but also which category of filer you fall under, which dictates the specific schedules and information you must provide. This proactive due diligence prevents surprises and establishes a clear roadmap for your ongoing compliance, turning potential confusion into a precise, actionable strategy.

Protecting Your Business (Permanent Establishment)

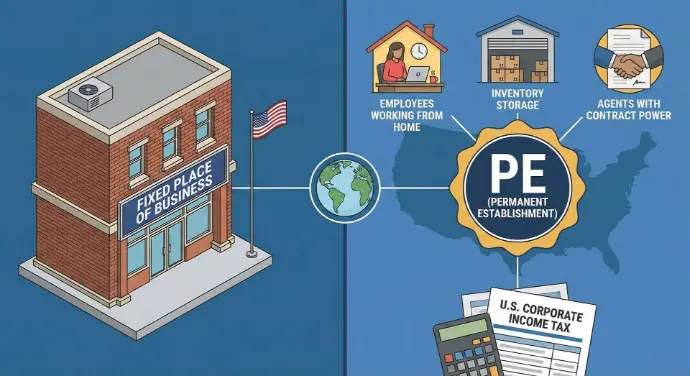

For SMB owners with operations or interests spanning the US-Canada border, merely complying with Form 5471 is just one piece of the puzzle. Your foreign corporation itself faces significant U.S. tax exposure that must be meticulously managed. One of the critical concepts demand your immediate attention: Permanent Establishment (PE). Failing to address these can lead to your Canadian company inadvertently owing U.S. corporate income tax, even if it has no physical U.S. office, creating unexpected liabilities and potential double taxation.

Permanent Establishment (PE) refers to a fixed place of business in the U.S. through which your foreign enterprise carries on business. This isn't just a brick-and-mortar office; a PE can be triggered by seemingly innocuous activities like having employees regularly working from home in the U.S., storing inventory, utilizing agents who can bind your company to contracts, or even a prolonged project in the U.S. If your Canadian corporation is deemed to have a PE, its profits attributable to that PE become subject to U.S. corporate income tax, alongside its Canadian obligations. Strategic planning involves structuring your U.S. activities to avoid inadvertently creating a PE or, if one is unavoidable, understanding and mitigating its tax implications through expert treaty analysis.

The Power of Integrated, Evolving Compliance Protocols

Cross-border tax planning isn't a static, one-time exercise; it's a dynamic, ongoing process that requires continuous vigilance and adaptation. Your business operations evolve, life circumstances change, and tax laws in both the U.S. and Canada are constantly being updated. Relying on outdated advice or a set-it-and-forget-it approach to compliance is a recipe for future problems and potential penalties. The truly effective strategy lies in establishing integrated, evolving compliance protocols.

This means continuously monitoring your corporate structure, financial transactions, and any changes in your personal residency or ownership stakes that could impact your Form 5471 obligations. It ensures that not only Form 5471 itself, but all its intricate and essential schedules, are filed accurately and on time each year. This includes reporting on income, earnings and profits, accumulated earnings, transactions with related parties, and any organizational changes. For U.S. persons who are also Canadian residents, this may also involve coordinating with Canadian reporting requirements, such as Form T1135 for reporting specified foreign property, ensuring a holistic approach to your international tax footprint. A robust compliance strategy anticipates these changes, integrates them into your annual reporting cycle, and proactively shields you from the ever-present risk of non-compliance.

Cross-Border Tax Expert Guidance Matters

Cross-border tax planning is complicated, not a DIY project. The stakes are too high, and the nuances of Canadian and US tax laws, combined with the complexities of the tax treaty, are too great for generalized advice or online guesswork. A seasoned cross-border tax strategist can help you accurately determine your residency status, calculate and mitigate departure tax, navigate withholding taxes, and ensure all necessary forms (like T1161) are filed correctly and on time. At MFI, we translate jargon into clear, actionable advice, building a robust compliance strategy that protects your wealth and provides a clear roadmap for your financial future in Canada and the US. Don't let tax anxiety overshadow your new beginning – empower your move with expert cross-border tax planning.

Book Your Initial Cross-Border Tax Consultant